2 in 5 UK retirees have retirement regrets, according to a Canada Life survey. If you’re saving towards your future, you could learn some valuable pension lessons and avoid repeating the same mistakes.

Securing the retirement you want often means thinking about this milestone many years before you celebrate it. One of the key challenges is balancing your financial needs and goals now with your long-term ones. Retirement regrets indicate it’s something many people struggle with.

So, if you’re still working and saving for retirement, here are three lessons you could learn from older generations.

1. 17% of retirees wish they’d increased pension savings while working

The Canada Life research suggests one of the biggest retirement regrets is simply not saving enough – 17% of those surveyed said they wished they’d increased their pension contributions. Similarly, 12% said they regret not making lifestyle adjustments earlier in life to allow them to save more for their later years.

While auto-enrolment means you’re likely to be paying into a pension if you’re an employee, simply paying the minimum contribution may lead to a pension pot that falls short of your expectations.

Indeed, a report from the Phoenix Group, noted: “There is widespread consensus that current auto-enrolment contribution rates are unlikely to provide an adequate retirement income for most savers.”

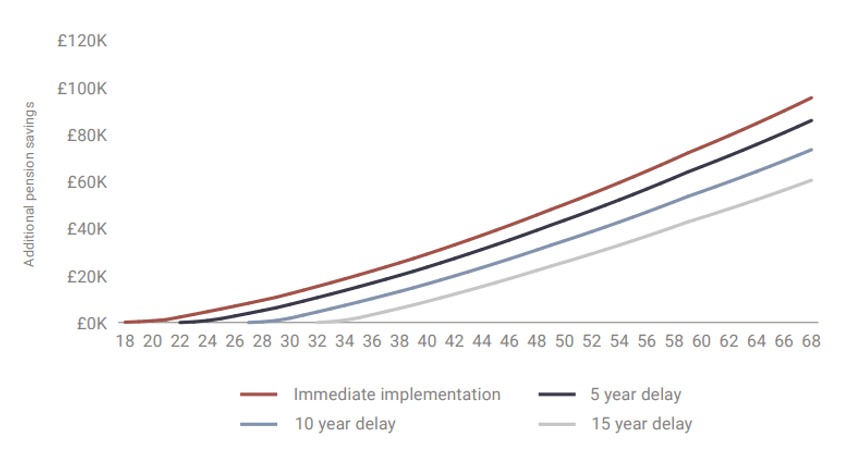

The report advocates increasing the default pension contribution rate from 8% to 12%. While the current government hasn’t indicated that it plans to do this, you can choose to increase your contributions, and some employers also offer higher pension contributions as part of their benefit package.

As your pension is often invested and benefits from compounding over a long time frame, reviewing your contributions now could mean the extra money really starts to add up.

The report notes that changing the minimum contribution level to 12% now could lead to a typical 18-year-old today having an extra £96,000 in their pension at retirement. However, as the graph below shows, delaying by even five years could lead to significantly less.

Source: Phoenix Group

Having a clear goal can be useful if you want to ensure you’re saving enough – how much do you need in your pension at retirement to live the lifestyle you want? From here you can work backwards to understand how much you need to contribute to your pension to make your goal more achievable.

Of course, setting a pension pot target isn’t always straightforward. You’ll often need to consider areas like life expectancy, inflation, and investment returns. Working with a financial planner could provide you with a tailored retirement plan that considers these factors.

2. 43% regret not accessing advice or guidance

Separate research from Standard Life found that more than 4 in 10 retirees regret not accessing advice or guidance either at the point of retirement or when they were still working. The survey results found:

- 51% wished they had more information about how to plan and prepare for their retirement

- 42% said they should have sought advice or guidance to plan for their retirement

- 37% said they should have sought advice or guidance before they accessed their pension savings.

You don’t have to be nearing retirement to benefit from professional financial advice. Seeking advice ahead of retiring could be useful throughout your career.

A tailored retirement plan could help you assess what steps you may take to improve your financial wellbeing once you stop working, and regular reviews provide an opportunity to see if you’re on track and what adjustments you might make.

3. 8% of retirees say they would have retired later than they did

Perhaps surprisingly, the Canada Life survey revealed that 8% of retirees wish they’d retired later than they did.

For some, this regret may come from wishing they’d delayed retirement so they could contribute to their pension for longer and enjoy greater financial security now. Yet, the report notes that others wished they’d worked for longer due to the potential mental health benefits.

Work can provide a structure and sense of purpose that some people miss once they retire. Phasing into retirement by slowly reducing your hours or taking a less demanding role could help you strike a work-life balance that suits you.

Incorporating your lifestyle goals into your retirement plan, rather than simply focusing on the numbers, could be useful too. Considering how you’ll fill your days in retirement and what will continue to make you happy might mean you’re less likely to live with regrets.

Get in touch to start planning for your retirement

It’s never too soon to start thinking about your retirement. In fact, taking control of your retirement plan sooner could mean you have more options, enjoy the retirement you’re looking forward to, and offer peace of mind during your working life. Please contact us to arrange a meeting to discuss your retirement plan.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.